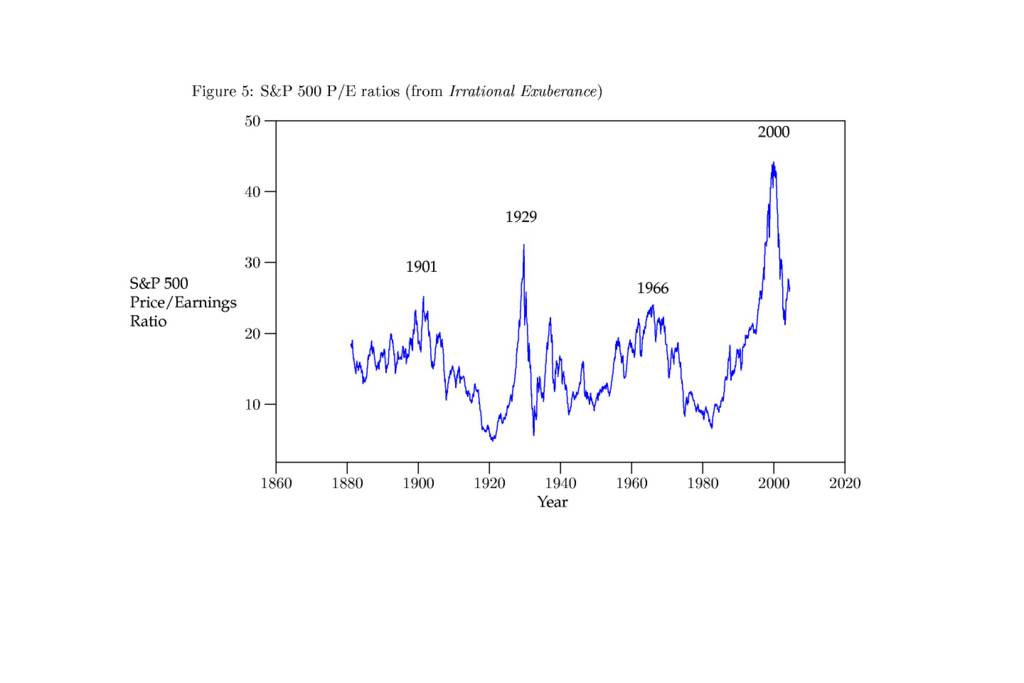

I recently finished Irrational Exuberance by Robert J. Shiller which suggested in 2000 that the U.S. stock market was overvalued. And of course, it was. Dr. Shiller suggests that people overvalue the market (defined by high price to 10 year average earnings ratios), when they think the old rules no longer apply. For instance, in 1929 people thought new technology, easy credit and popular interest in investing meant that high P/E ratios were sustainable.

It doesn't take much in the way of mental gymnastics to imagine each of these things being said in 1999. The Internet, Globalization, and Mutual Funds seemed poised to sustain higher earnings growth than anyone could have imagined 5 or 10 years earlier. (The book discusses lots of factors that contributed to bubble valuations, but these are the ones I remember having an impact on me -- right at the start of my investment experience.)

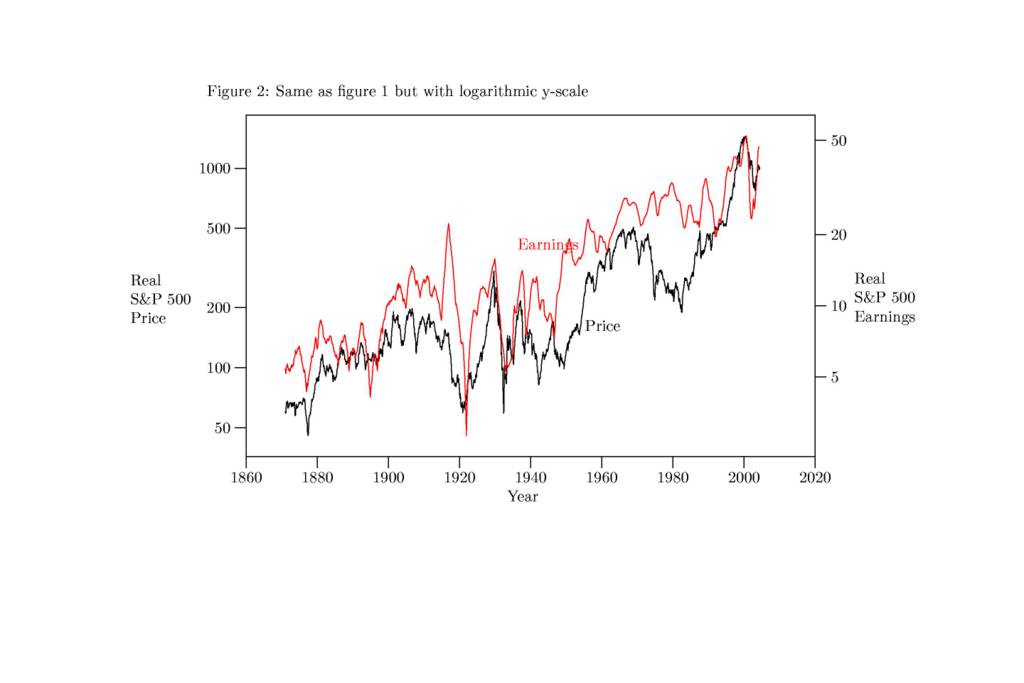

One of the most striking parts of the book, is a graph showing the rise of stock prices and earnings (as represented by the S&P 500 index) over the last 130 years or so. I've reproduced the figure below. It shows earnings increasing at a moderate rate and prices jumping all over the place. Especially interesting are the booms in the 1920s and 1960s followed by busts in the 1930s and 1970s. From 1982 to 2000 the divergence begins to look especially ludicrous. It sure looks like prices are headed south, despite the recent drop.

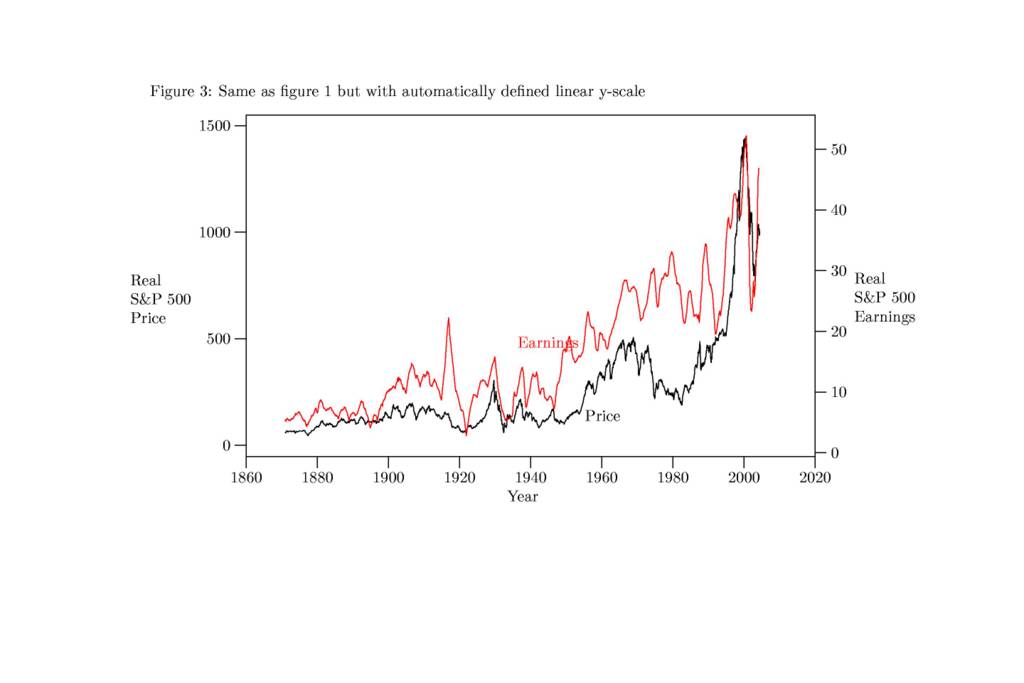

But there are a couple of problems with this graph. The tipoff is the scales on the left and the right. The left (price) goes to $1500[1] and the right (earnings) goes to $600, but there is no indication how those scales were chosen. Obviously if both lines were on the same scale, earnings would look nearly flat (since earnings are anywhere from 5 to 45 times smaller than prices). But if we are going to look at different scales, why not pick a scale that matches the range of earnings, say $0 to $55? One problem, from the point of view of selling the book's premise, is that prices wouldn't look so dramatically high.

Another issue is that the scale is linear. Even adjusted for inflation, S&P 500 prices and earnings are several orders of magnitude greater now than they were in 1871. On a linear scale, a large move percentage-wise is more dramatic when prices are high and muted when prices are low. If you have a $1000 invested that looses 10%, you're down $100 whether the price per share is $10 or $100. But if you put both changes on the same linear scale, the drop from $100 to $90 is more dramatic than the drop from $10 to $9. One way to correct for this illusion is to use a logarithmic scale. I've used the same data to created a corrected version of the chart.

I'm not saying that Dr. Shiller is wrong or trying to mislead, but this chart is misleading. Earnings and prices don't fit on the same scale, but putting them on the same graph suggests a relationship between them. Implicit in the original graph is the suggestion that P/E ratios should be around 2.5 (since 1500/600 is 2.5). Using a linear graph and letting the graphing software determine the range suggests a P/E ratio of about 27. (Linear graphs are better for accurately determining absolute values.) That's skewed by very high ratios in the last few years.

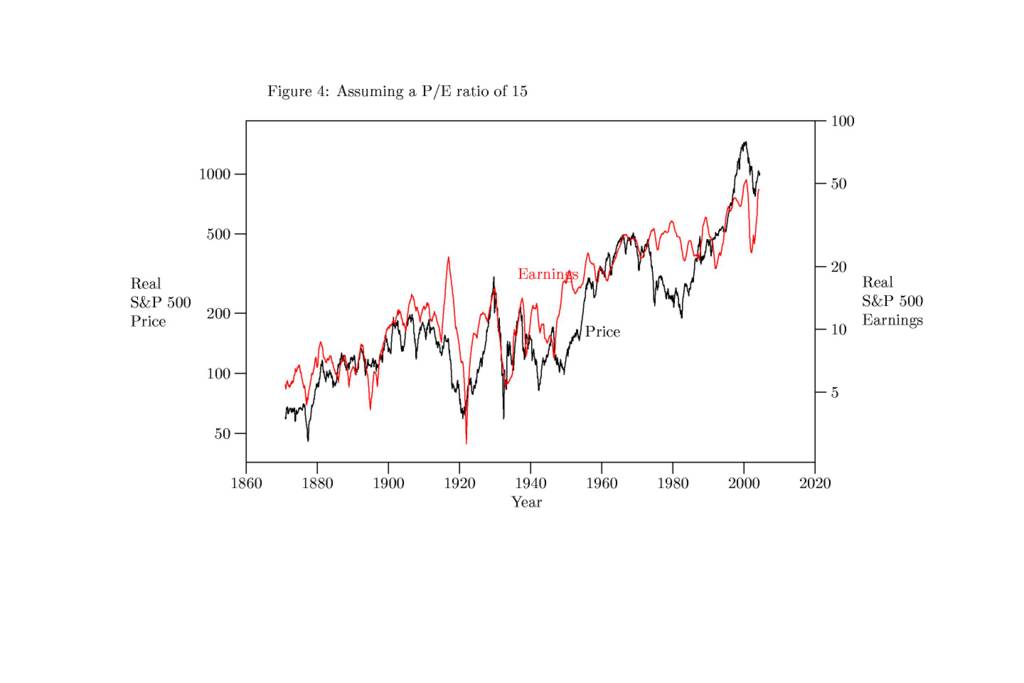

And this is the frusterating aspect Irrational Exuberance -- it makes a strong case that the market was overpriced in 2000, but it doesn't spend much time discussing the fair value of the market. The historical average is about 16 which is again skewed by recent history. I've produced another chart assuming a fair P/E ratio of 15. Years in which the Earnings line ducks under the Price line (such as 2000) would be years when the market is overvalued. Maybe this ratio is fair and maybe it isn't.

A practical question for me, right now, is whether or not the S&P 500 index is overpriced at a P/E of 18. I think it might be.

Footnote:

[1] I noticed after I made the graph that the original goes to $1600.